COMP Q1: They Did It

Bull Case Back on the Table as COMP Beats, Raises and Guides Above Street

May 5th, 2026

Lake Cornelia Research Management, Inc.

Note: Please read the disclaimer and risk disclosures at the end of the memo before preceding.

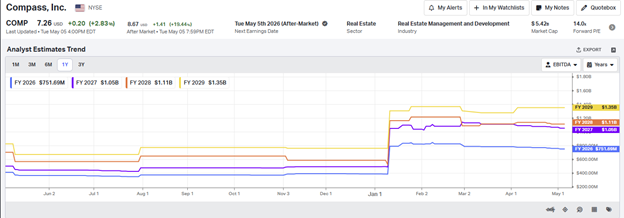

We have written extensively on COMP (links below to prior notes). The stock has been a struggle since the merger close, falling from ~$13 to $7. 2026 is set to be a transition year for the company as cost to achieve synergies consume most cash flow. Additionally, macro pressure on oil and rates is perceived to limit upside in housing transactions. Factoring in the higher balance sheet leverage that came with the deal for HOUS, investors have been in a wait and see mode. Sell-side numbers have come down somewhat since the Q4 call (they will go back up now).

COMP is up ~20% after-hours on a beat and raise Q1. Synergy guidance was increased and the call was extremely positive.

The Punch Line

We said from the beginning that COMP could do $2+ billion of EBITDA in a moderate upcycle. We were pleased by this discussion on the conference call:

In our investor deck this quarter, we have provided a scenario analysis to demonstrate how we are positioned to generate resilient financial performance, even in a flat housing market, and capture significant upside as the market improves and once we realize our cost synergies. Importantly, these scenarios assume no agent adds, no organic share take, no margin improvement, no improvement on T&E or mortgage attached, or any contribution from leads or other ancillary revenue streams, which we view as incremental growth levers in our business beyond the housing recovery. I also want to emphasize that this is not guidance, but these scenarios should help provide a range of expectations around the earnings power of our combined company simply from an eventual recovery in existing home sales and once we’ve realized our cost synergies, specifically assuming the housing market remains flat at 4.1 million existing home sales, we would generate roughly $1 billion in adjusted EBITDA and $750 million in unlevered free cash flow. In the next scenario, which we’ve assumed as 4.8 million existing home sales for this analysis, we would generate $1.5 billion in adjusted EBITDA and $1 billion in unlevered free cash flow. At mid-cycle levels of 5.5 million home sales, we would generate $2 billion in adjusted EBITDA and $1.5 billion in unlevered free cash flow. And lastly, we also provided an upside scenario of 6 million home sales and at those levels, we would generate $2.5 billion in adjusted EBITDA and roughly $2 billion in unlevered free cash flow. So, what you can hopefully see from this analysis is that one, even at 4.1 million existing home sales, which we believe is the trough of the cycle, we could -- we would expect the business to generate $750 million in a levered free cash flow, giving us confidence that we can make progress in reducing leverage even in conservative scenarios and two, once we begin the recovery up to mid-cycle levels, that the earnings growth and free cash flow potential in this business is incredibly significant.